Did you know that properties configured as HMOs can command up to 35 percent higher rental yields compared to standard single-tenancy homes? For many investors, this potential comes with a host of complex valuation challenges that often get overlooked. With evolving regulations, specific room layouts, and rising compliance costs, the true value of HMO properties requires deeper analysis than most realize. Clarifying these factors can mean the difference between a profitable investment and costly mistakes.

Key Takeaways

| Point | Details |

|---|---|

| Understanding HMO Valuation | HMO valuation goes beyond traditional methods, requiring insights into financial potential and regulatory landscape. |

| Valuation Methods | Key methods include comparative market analysis and income capitalization, each providing distinct insights for different property types. |

| Legal and Licensing Requirements | Compliance with licensing laws is critical, as failing to adhere can lead to significant financial penalties and affect property value. |

| Risks and Costs | Investors should conduct thorough due diligence to navigate regulatory challenges, initial setup costs, and the complexities of multi-tenant management. |

Defining HMO Valuation and Common Misconceptions

HMO valuation represents a sophisticated property assessment technique that extends far beyond traditional real estate appraisal methods. More than simply measuring physical structures, it provides investors with critical insights into a property’s comprehensive financial potential by meticulously examining rental markets, potential occupancy rates, and unique room configurations.

Contrary to popular misconceptions, understanding what is HMO valuation isn’t just about calculating square footage or comparing market prices. According to research, HMO properties present complex investment opportunities that require nuanced evaluation:

- Multiple tenancy streams can reduce income volatility

- Higher compliance costs offset potential rental advantages

- Regulatory requirements significantly impact overall property value

Investors often mistakenly believe HMO valuations mirror standard property assessments. In reality, these evaluations demand specialized knowledge about:

- Local rental market dynamics

- Potential room configuration flexibility

- Anticipated regulatory landscape changes

- Compliance and safety investment requirements

Understanding these multifaceted aspects transforms HMO valuation from a simple numerical exercise into a strategic investment analysis tool.

Valuation Methods for HMO Properties

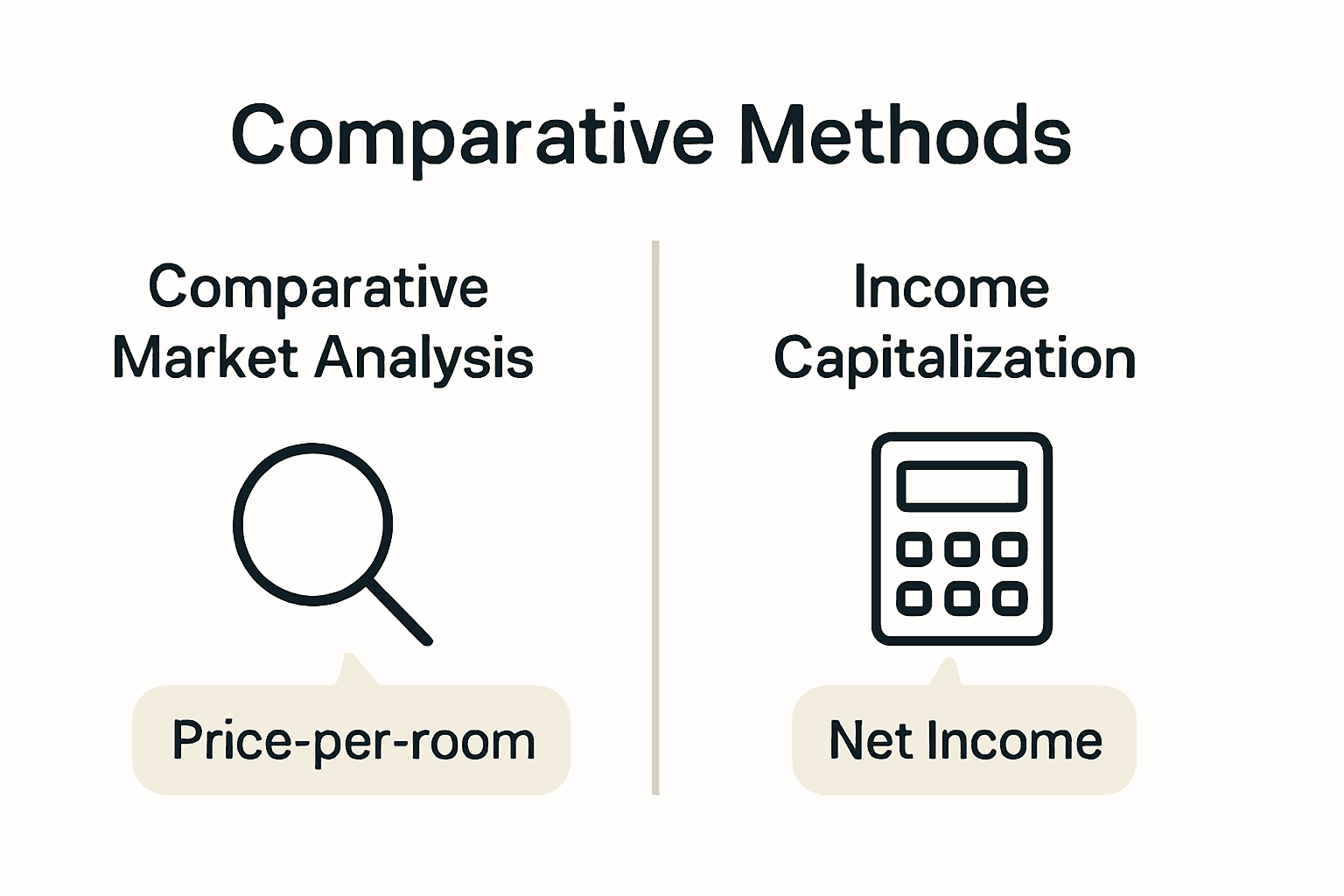

HMO property valuations rely on two primary assessment approaches that provide investors comprehensive insights into potential investment returns. According to research, these methods differ significantly from traditional residential property evaluations, requiring a more nuanced understanding of income generation potential.

The first method, comparative market analysis, examines similar HMO sales and market trends, calculating value through detailed price-per-room assessments. Understanding HMO property management strategies becomes crucial in this approach, as each room’s potential rental income dramatically impacts overall property valuation.

The second approach, income capitalisation, provides a more dynamic valuation technique by:

- Calculating gross rental income

- Deducting operating expenses

- Determining net operating income

- Applying a specific market yield

This method proves particularly effective for larger HMO properties where multiple income streams and operational complexities require sophisticated financial analysis.

Here’s a comparison of the two primary HMO valuation methods:

| Valuation Method | Key Features | Best Suited For |

|---|---|---|

| Comparative Market Analysis | Price-per-room approach Considers recent HMO sales Focus on similar properties |

Small to medium HMOs Areas with active sales data |

| Income Capitalisation | Calculates net rental income Accounts for operational expenses Applies market yield |

Larger HMOs Complex multi-let properties |

- Potential room configuration flexibility

- Regulatory compliance costs

- Market-specific rental demand

- Operational management expenses

Successful investors understand that HMO valuation is not just about current market value, but potential future income generation and strategic property optimization.

Essential Legal and Licensing Considerations

HMO licensing represents a complex legal landscape that can significantly impact property investment strategies. In the UK, properties with five or more tenants from multiple households require mandatory licensing, with regulatory requirements that extend far beyond simple paperwork.

Understanding the HMO licensing process is crucial for investors, as non-compliance can result in substantial financial penalties. Local authorities typically charge licensing fees ranging from £500 to £1,500 and mandate strict compliance standards:

- Minimum room size specifications

- Mandatory gas and electrical safety certificates

- Comprehensive fire safety measures

- Regular property inspections

Lenders and valuers often take a conservative approach when assessing HMO properties. They may:

- Reduce property valuation based on compliance issues

- Discount rooms if communal spaces are inadequate

- Ignore discretionary licensing

- Limit borrowing potential

Investors must recognize that legal considerations are not just bureaucratic hurdles, but critical components of successful HMO property management that directly influence investment value and potential returns.

Key Factors That Influence HMO Value

HMO property valuation is a multifaceted process that extends far beyond traditional real estate assessments. Property configuration plays a critical role in determining investment potential, with specific characteristics directly impacting overall market value and income generation capacity.

Understanding HMO investment strategies reveals that multiple interconnected factors influence property worth. The most significant valuation drivers include:

- Location proximity to universities, employment centers, and amenities

- Property condition and structural integrity

- Number and size of lettable rooms

- Potential rental yield

- Regulatory compliance status

Investors must carefully evaluate several key considerations when assessing HMO property value:

- Spatial configuration and room layout

- Potential occupancy rates

- Communal space quality

- Local market rental expectations

- Planning class restrictions

Unique market dynamics like Article 4 areas can further complicate valuations, potentially creating supply restrictions that incrementally increase property values over time. Successful investors recognize that HMO valuation is a nuanced art of balancing physical assets with potential income generation capabilities.

Investor Risks, Costs and Pitfalls to Avoid

HMO investments present complex financial landscapes where potential rewards are accompanied by significant challenges that can catch unprepared investors off-guard. Understanding these risks is crucial for maintaining profitable and sustainable property portfolios.

Completing thorough due diligence becomes paramount in mitigating potential investment pitfalls. The most critical risks investors must navigate include:

- Stricter regulatory compliance requirements

- Higher initial setup and licensing costs

- Increased property management complexity

- Potential tenant conflict management

- Accelerated property wear and tear

Investors should be particularly cautious about the financial implications of HMO investments:

- Substantial upfront fire safety modifications

- Comprehensive planning permission expenses

- More frequent maintenance cycles

- Higher insurance premiums

- Potential income volatility from multi-tenant arrangements

Successful HMO investors recognize that meticulous planning, comprehensive risk assessment, and proactive management are not optional extras but fundamental strategies for navigating this challenging yet potentially lucrative property investment sector.

Unlock Real Value from Your HMO Investment

If understanding HMO valuation feels overwhelming—from regulatory complexities to achieving accurate appraisals—you’re not alone. Many investors struggle to navigate the maze of compliance, room configurations and evolving market yields. This confusion puts your capital and rental income at risk, and can make the property selection process daunting. By tackling these issues head-on, AgentHMO removes uncertainty by connecting you with tools, market analytics and specialists focused exclusively on the UK HMO sector.

Ready to take action? Explore our platform for fast, expert HMO property valuations and discover vetted estate agents and property management solutions that put compliance and profit first. Whether you’re buying, selling or managing, visit AgentHMO to access a full suite of HMO support services and listings, or get custom guidance by browsing our expert directory of HMO professionals. The clarity and confidence you need starts today—secure your next HMO success now.

Frequently Asked Questions

What is HMO valuation?

HMO valuation is a property assessment technique that focuses on evaluating a property’s financial potential by examining multiple factors, including rental markets, occupancy rates, and unique room configurations.

How do you value an HMO property?

HMO properties are valued using two main methods: comparative market analysis, which looks at price-per-room based on similar sales, and income capitalisation, which calculates potential income after operating expenses to determine net operating income.

What are the legal requirements for HMO properties?

HMO properties with five or more tenants from different households require mandatory licensing, which includes compliance with minimum room sizes, safety certificates, and regular property inspections.

What factors influence HMO property values?

Key factors that influence HMO property values include location, condition of the property, the number and size of lettable rooms, potential rental yield, and compliance with regulatory requirements.